The End of One-Factor Crypto

Why BTC price is no longer the variable that matters most

Historically, crypto has traded as one Bitcoin-sensitive factor. That era is ending.

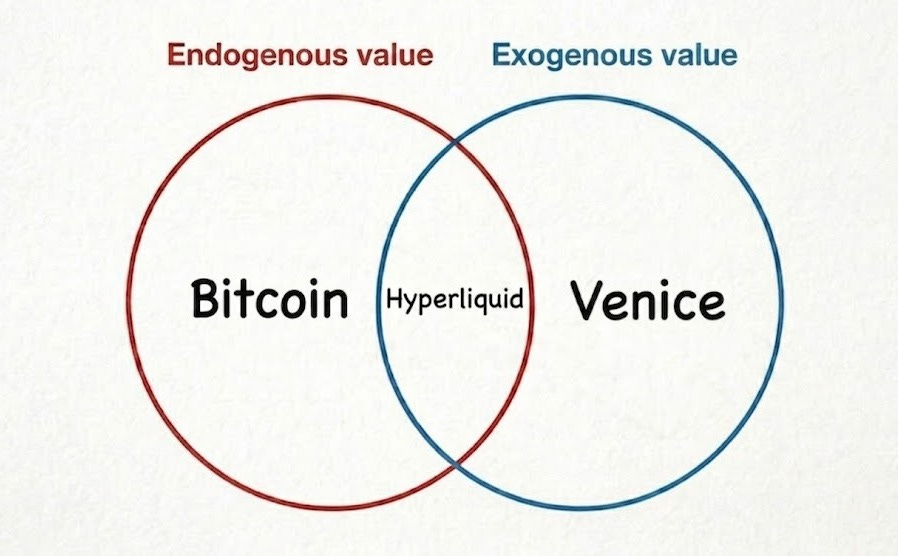

The crypto economy is bifurcating into two groups: endogenous and exogenous.

The former is the crypto of old: tokens and projects whose value depends on crypto prices. The latter is crypto in name only, with value increasingly exogenous to crypto prices.

Bitcoin's value comes from its properties and reflexively from its price. A rising price reinforces the perception of the properties. At the peak of a bull market, Bitcoin is perceived to be interplanetary money, the most scarce digital bearer instrument known to mankind. At a bear market bottom it's dismissed as a cashflow-less digital collectible.

Hyperliquid sits in the middle. Much of its business still depends on crypto prices, but both the supply and demand sides are broadening. A lot of on-chain financial infrastructure sits here, with the assets underneath shifting toward tokenised real-world assets.

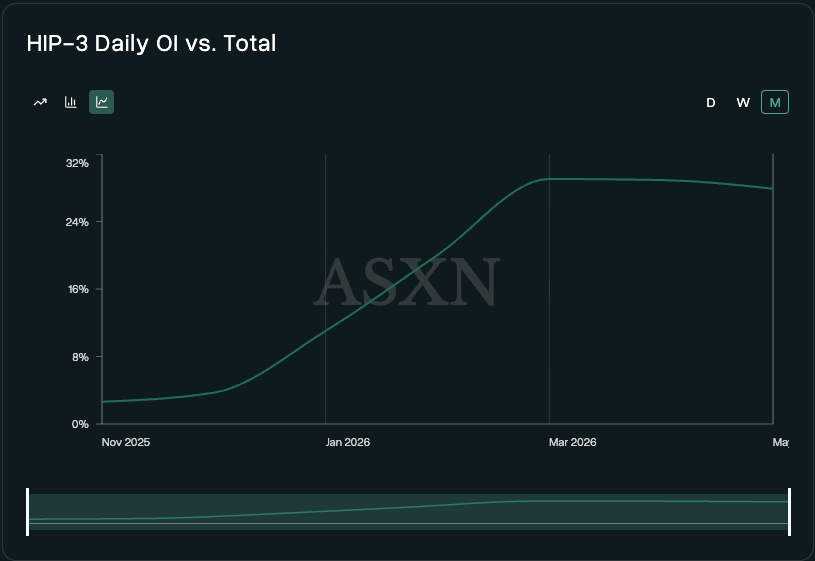

HIP-3 Open Interest is a rough proxy for non-crypto-related Open Interest. The percentage of total Hyperliquid Open Interest attributable to HIP-3 sits at ~30%, up from ~4% in November 2025. HIP-4 (outcome markets) should widen this further, pulling in new demand (traders) and new supply (markets, assets) at once.

On the purely exogenous side, the driving forces for a project like Venice are completely exterior to the crypto market. Customer profiles overlap, but the business model looks a lot more like consumer AI than something like Uniswap. The latter still largely relies on users trading assets with endogenous value, making its business downstream of the price of these assets. Venice packages private multi-modal inference into a usage-plus-subscription model.

The only crypto connection is the choice of a token as the instrument that captures business value, plus the fact that some of its inference suppliers happen to wear crypto labels. Perhaps also the crypto-native understanding of Venice’s steward Erik Voorhees that tokens can be an excellent marketing tool when done well.

Figure is an easy example on the listed equity side, a fintech lender using its own chain to cut home equity approvals to under five minutes. The blockchain is incidental, the business is the point.

The emergence and growth of the exogenous class at scale in listed equity and token markets is meaningful. Historically, pure bottom-up investing has been difficult given the high sensitivity of most business models to crypto prices. It’s not as though crypto hasn’t had exogenous narratives before; every "blockchain not Bitcoin" cycle promised them. It’s mostly that they collapsed back into crypto-beta because the demand never showed up, the revenue wasn't there (if it was, it was not captured by the token), and once the token stopped going up there was nothing underneath.

What's different this time is that you can answer who pays and why, the demand is measurable and less reflexive in many cases, and the token as an instrument is slowly improving (more on that later). Venice signup revenue is real money from users buying inference. There's no obvious reason it reverses when crypto draws down, because it was never a function of prices. You have two things that prior cycles lacked: usage that persists, and buyers underwriting on fundamentals rather than solely narrative.

Take for example the stablecoin corner of private markets. In March 2026, Mastercard agreed to buy BVNK for up to $1.8bn, fifteen months after BVNK's Series B closed at a $750m valuation. Bridge (bought by Stripe for $1.1bn in February 2025) is reportedly growing 4x year-on-year inside Stripe per their annual letter. None of this tracks the crypto cycle.

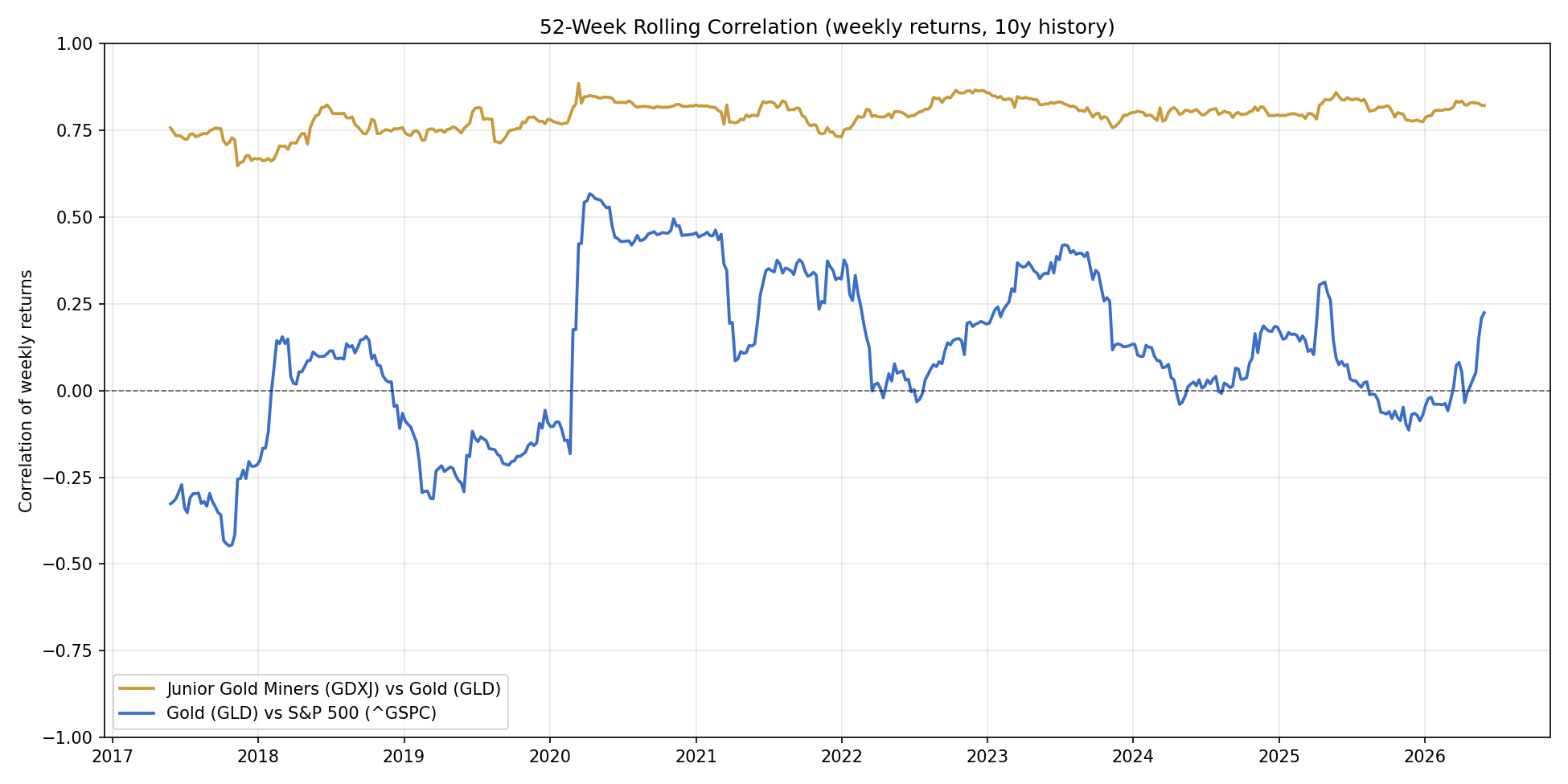

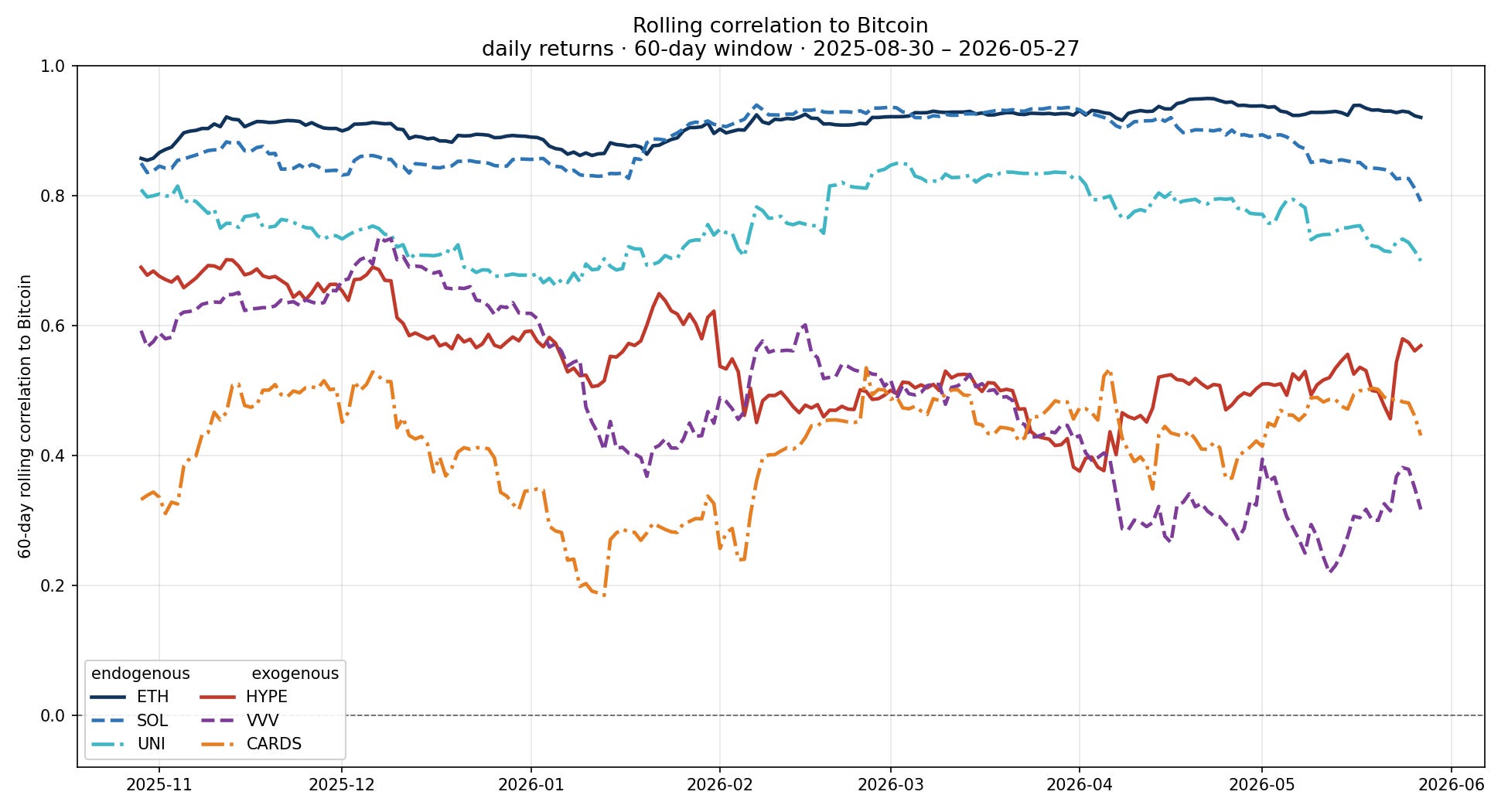

This isn't a bearish call on the endogenous category. Just as gold and even junior gold miners might have their time and place in a portfolio, there’s a time and place for something like BTC and the endogenous class, but fundamentally different drivers will likely continue to bifurcate performance and correlations. You can see both relationships in the data:

The analogy made literal. Junior gold miners track gold at a correlation that never really leaves the ~0.75 region. That’s how crypto broadly trades today: junior miners to Bitcoin’s gold, levered bets on the same underlying. The blue line is the other relationship. Gold and the S&P share some macro weather but trade on their own drivers. That’s the destination for the exogenous class. Over time these names should migrate from the gold line to the blue line, from levered proxy to independent assets that occasionally share the weather.

Much of the “endogenous class” still moves closely with Bitcoin. A few exogenous names sit lower, but the window's too short to mean anything yet. Fundamentals change first; the correlations follow.

This changes the analytical approach. The exogenous class needs underwriting like a normal business: who pays for the product, how the unit economics work, where the moat sits. BTC price stops being the most important variable and you start sounding like a fintech investor with weird custody.

Exciting “exogenous” categories, in no particular order and with miscellaneous notes attached:

on-chain exchanges and brokers

credit/redemption solutions for longer-tail tokenisation (Grove Basin looks interesting here)

real crypto x AI (private inference, distributed open-source model training à la Psyche by Nous Research)

neobanks (I tend to like the more privacy-focussed players like Payy and Raycash, the programmable privacy infrastructure, Aztec and Zama, that enables them is also interesting)

lending (Morpho is becoming the institutional standard for repo-like markets, smaller names like Valinor and 3jane target interesting niches in private credit)

stablecoin and real-world asset/tokenisation issuers

payment rails (Stripe w/ Tempo the incumbent to beat in broad payments rails; in agent-payments it’s Coinbase, for now)

non-finance consumer crypto (products like Venice and Collector Crypt come to mind, unique cases where imbuing a token with value derived from a non-crypto business can drive marketing value and adoption)

agentic economy (the prize is agent<>vendor/creator coordination at the access layer which is less substitutable than the rail. Cloudflare is well placed, but whether it taxes the flow or just sells the toggle is the open question)

Most durable exposure to this theme is equity today, not tokens. Good tokens are the exception and will only earn a larger role if the instrument improves, which sits with regulators and industry. There's progress on both, CLARITY on the regulatory side and transparency efforts from the likes of Blockworks on the other. The token has a lot of work to do.

None of that changes the main point. The driver is shifting from one factor to many, the work is no longer reading the Bitcoin chart but underwriting businesses. Don’t spend the next decade confused about why “crypto” stopped moving as one.