Positioning for Polymarket

A Practitioner's Guide

At a roughly $8-10 billion private valuation, there are two ways to get exposure to Polymarket: buy in at those terms or farm your way in at a fraction of the cost.

I chose the latter. Not because I’m bearish on Polymarket; volumes have surpassed the November 2024 election highs, NYSE’s parent company took a $2 billion stake, and their CMO effectively confirmed a token on a podcast in October 2025: “There will be a token, there will be an airdrop.” I chose it because farming allows you to build exposure to a potentially highly valued token at a small to negative cost while retaining optionality and liquidity. At current private valuations, a lot of the positive sentiment looks to be already priced in.

Given the reliance on UMA from an oracle standpoint and Polygon from a chain standpoint, it’s not hard to imagine the case for $POLY token utility either. And with competition heating up; Kalshi growing its regulated offering and Hyperliquid sitting on significant $HYPE supply available as incentives if they choose to pour fuel on HIP-4, Polymarket’s incentive to launch a token is only increasing.

Roughly six months in, with plenty of pivots and dead ends along the way, this is a practitioner’s guide to how I’ve been positioning.

Eligibility

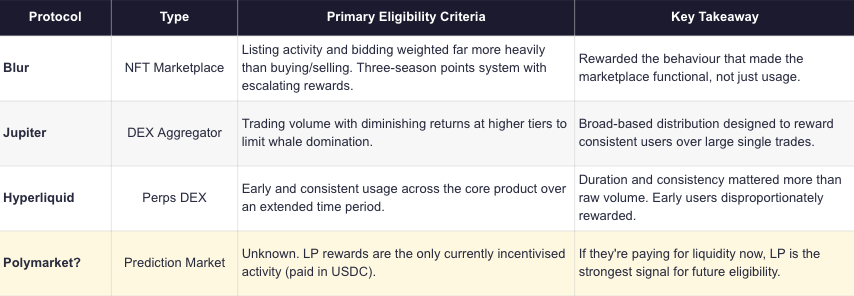

Historical precedent tells us that heavy, consistent and early usage across the core product is what counts when it comes to airdrop eligibility. In the context of Polymarket there are a few different ways to measure usage: making a deposit and holding a balance, active months/weeks/days, trading volume, number of trades, number of markets traded, PnL, and liquidity provision (limit orders filled, limit orders placed, and Liquidity Rewards earned).

Eligibility likely combines some of these factors. The most pertinent question is which matters most. Historical precedent offers some guidance:

The common thread: protocols reward the behaviour they need most. For a prediction market, it’s liquidity.

We can simply listen to what Polymarket are telling us. Liquidity provision is being incentivised in the form of Liquidity Rewards, whereby LPs are paid USDC to provide liquidity based on certain criteria. If they’re incentivising it now with USDC, what’s the chance it gets rewarded heavily in airdrop eligibility and perhaps $POLY rewards when the time comes?

This incentivisation makes sense. Without deep order books and tight spreads the product is basically unusable. Retail want to get the price they see. Institutions want to express views with meaningful size and get out if they need to. Commentators want to cite odds from thick markets where the price is real and not the midpoint of a 10c spread with a few thousand dollars either side.

The approach to date

Despite a bias towards liquidity provision in terms of eligibility maximisation, my initial framework was simpler (as outlined in the initial piece I wrote about Polymarket farming last October):

Make economically rational decisions in a vacuum; decisions that make sense even if the airdrop never happens but which offer large asymmetric upside if the thesis is correct.

Or more plainly: don’t burn money chasing an airdrop that might never come, or one you might not qualify for.

The approach centred on making a real absolute return while organically generating activity across many of the metrics listed above. For the most part this involved buying high probability markets (FOMC decisions, betting against insolvencies/depegs etc.) along with making a handful of crypto-focussed TGE valuation bets.

All in all the results have been acceptable, generating roughly ~7% over 6 months on the capital deployed, around 14% annualised without factoring in any potential airdrop eligibility generated.

Despite a relatively small allocation to this strategy (~4% of book), it has generally been difficult to achieve high utilisation of the capital, limited by the opportunity set and often-times poor liquidity on more niche markets such as the TGE valuation bets.

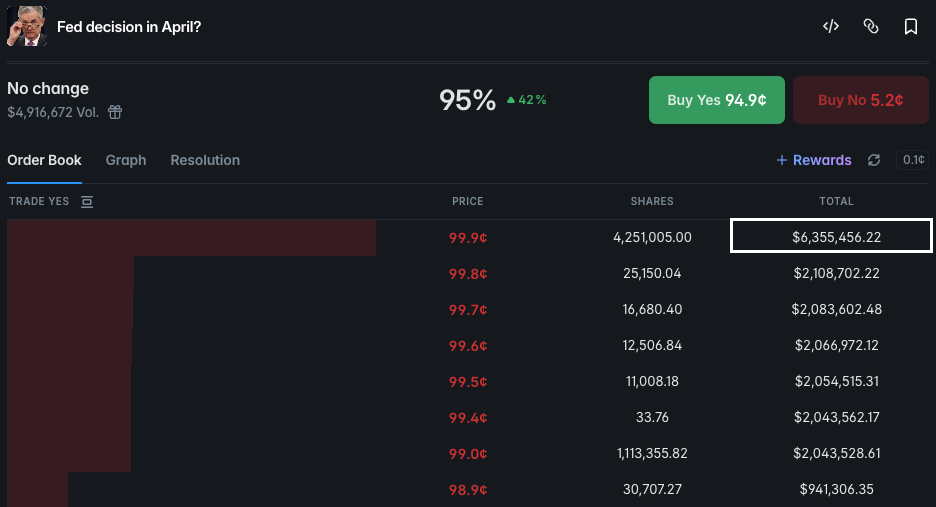

This led to exploring the possibility of automated strategies that could generate high levels of activity with relatively small levels of capital. When manually placing orders I noticed that very often there would be an abundance of liquidity right at the extreme of the pricing range (99.9c):

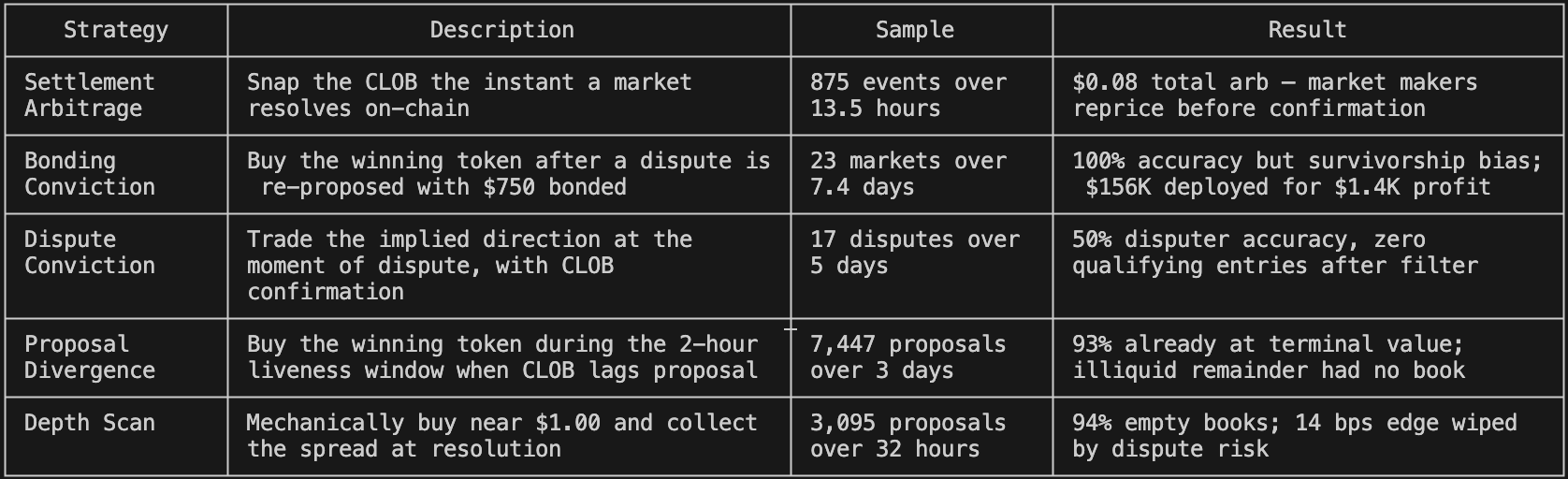

I began to wonder whether I could capitalise on stale limit orders closer to the resolution or at the resolution of these markets. The great allure of risk-free arbitrage...

UMA resolves markets through a multi-step on-chain process (proposal, optional dispute, final settlement) with each step involving real money (disputers bond 750 USDC, proposers stake capital on outcomes). Surely, somewhere in that lifecycle, the oracle knows something the order book hasn’t priced yet.

I spent the better part of three weeks on this. Mapping the oracle lifecycle, monitoring the mempool, writing scripts to detect timing gaps between settlement events and order book repricing. It felt like the kind of inefficiency that could exist in a fairly immature market.

It doesn’t.

The reason is straightforward: market makers are sophisticated and are monitoring the mempool for pending oracle transactions to reprice orders before those transactions confirm on-chain. By the time a settlement, proposal, or dispute event is visible, the order book already reflects it.

Whenever I found a genuine gap between the oracle and the CLOB, it was on a market nobody was trading: obscure golf markets, niche soccer goalscorer markets, esports etc. The pattern was the same everywhere. If a market had enough liquidity to make the arbitrage worthwhile, the market makers had already priced the oracle event. If they hadn’t, there was nothing to trade against.

Every path that tried to extract edge from the resolution side came up short. Which is what pointed me back towards providing the liquidity itself.

Burn to earn: the pivot to LP

Despite leaning towards liquidity provision as the likely apex predator of airdrop eligibility, my initial reservation was that I expected it to be a negative expected value activity. My goal was to make money while generating potential eligibility as a by-product. Paying to provide liquidity felt like the kind of trap that separates smart farmers from desperate ones.

")

My viewpoint changed when I saw the remarkably low barrier to being a top LP as measured by liquidity rewards. As of February 2026:

972 wallets have earned over $1,000 in rewards

4,429 wallets have earned over $100

16,109 wallets have earned over $10

38,028 wallets have earned over $1

Out of 2.18 million wallets, less than 2% have generated more than $1 in rewards. If liquidity provision is prioritised in terms of eligibility, and everything Polymarket is telling us suggests it will be, top LPs represent a very small cohort. A tiny percentage of wallets could stand to be beneficiaries of a disproportionate share of token supply.

Reframing the economics

The question then becomes: what is the minimum I need to spend to build a credible LP footprint, and is that cost justified by the expected value? Think of it like buying a Pendle YT: you’re paying a known cost for exposure to an unknown upside, and the maths only need to work out roughly right for the trade to be good.

The approach became clear: take the cumulative profits earned from the initial directional strategy as a starting balance, re-allocate the principal elsewhere (partially solving the capital utilisation problem), and use LP rewards as a subsidy to fund presence across many markets simultaneously. No intention to profit from market-making but to minimise the net cost of maintaining qualifying LP presence for as long as possible, across as many markets as possible.

This is a fundamentally different optimisation target to traditional market-making. We want wide spreads (just tight enough to qualify for rewards), minimal fills (we assume every fill is adverse selection), and we accept negative PnL within a pre-defined budget. The metric that matters is the ratio of LP footprint to capital burned in achieving it.

How Liquidity Rewards work

Polymarket’s reward formula scores each qualifying limit order based on proximity to the midpoint and size, with a quadratic penalty for distance. For example, an order at half the maximum qualifying spread scores only 25% as much as one right at mid. Crucially, it rewards two-sided liquidity: your effective score is roughly the minimum of your bid and ask scores. A lopsided book scores poorly no matter how much capital you have on one side.

score = ((max_spread - order_spread) / max_spread)² × size

Your share of a market’s daily reward pool is your effective score divided by the sum of all qualifying LPs’ scores. More competition means smaller slices, which makes market selection as important as quote placement.

The approach: minimum viable presence

With rewards economics understood, the strategy becomes an optimisation problem: maximise breadth and consistency of LP presence while minimising capital at risk and adverse selection losses.

In practice this means quoting symmetric two-sided orders across a portfolio of reward-eligible markets, sized at the minimum qualifying threshold with a small buffer rather than trying to capture meaningful reward share in any single market. We’re not competing with professional market makers on execution speed or pricing accuracy. We’re competing with other airdrop farmers on consistency, breadth and patience.

Market selection is the most consequential decision. Polymarket typically has 30,000+ active markets but reward pools and competition vary enormously. The scoring heuristic is intuitive:

Controlling the burn

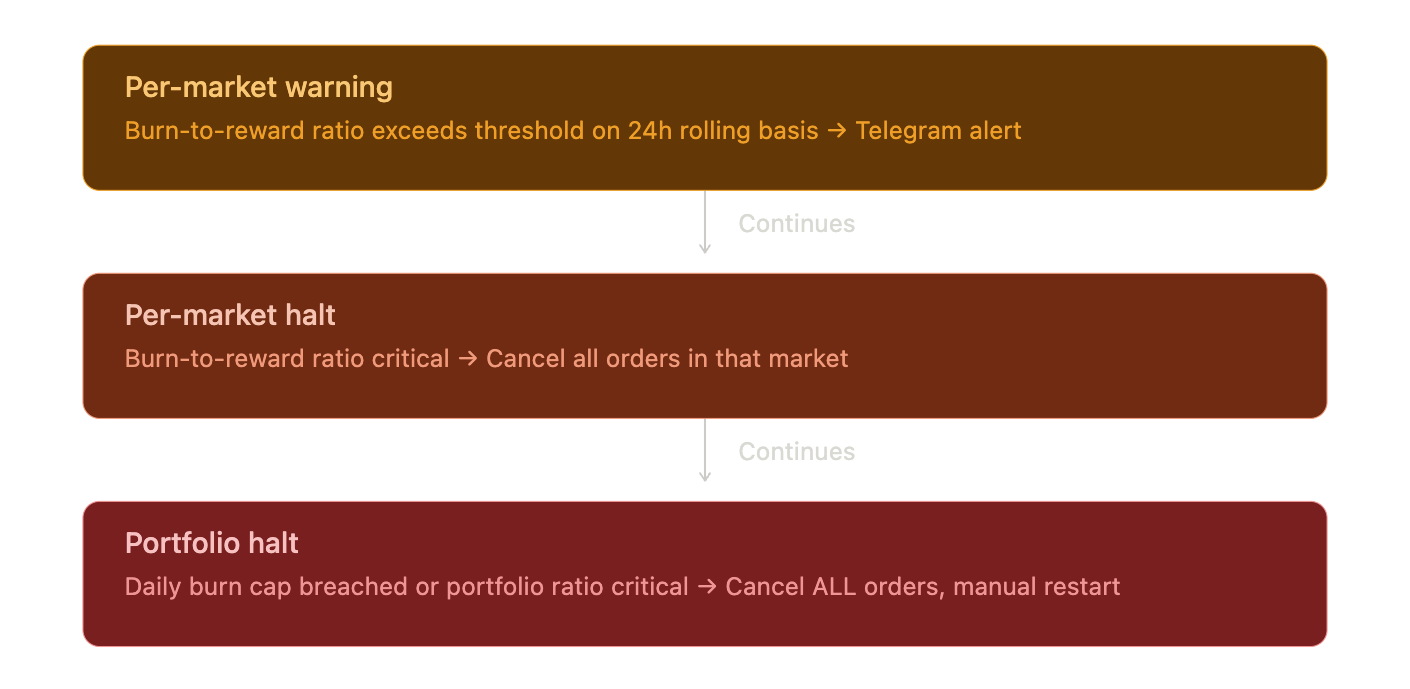

Risk management operates at multiple levels. Individual markets are monitored on a rolling burn-to-reward ratio: if the cost of adverse selection in a given market starts running meaningfully ahead of the rewards it generates, the market gets flagged and eventually halted. At the portfolio level, a hard daily burn cap acts as a backstop where even a catastrophic day stays survivable, giving the strategy a long runway.

Additional protections layer underneath such as anomaly detection on individual fills, inventory limits, and automatic wind-down near resolution but the daily burn cap is the one that matters most. We can tolerate burning slowly and predictably. We cannot tolerate burning quickly and unexpectedly.

Risks

There are several ways this trade fails:

The token never materialises. Despite the CMO’s comments and the broader trajectory, there is no binding commitment. Polymarket could delay indefinitely or decide that a token doesn’t serve their interests. If this happens, the capital burned on the LP strategy represents an absolute loss.

Opportunity cost. Capital deployed to LP on Polymarket is capital not deployed elsewhere.

Beyond these, there are several secondary risks worth noting. Eligibility criteria could underweight LP in favour of volume or number of markets traded, though the activity generated in the earlier directional phase provides some hedge. Sybil filtering could be aggressive enough to catch multi-wallet operations but genuine cross-strategy trading history should differentiate. And adverse selection could exceed burn budget in a particularly volatile period, though the circuit breakers and daily caps are designed to make that a slow leak rather than a blowout.

Expected Value

A rough scenario sketch makes the asymmetry tangible. Assume a conservative 5% of supply distributed to users at an $8 billion FDV: that’s $400 million. Now assume LP-weighted activity receives 30% of that allocation (a reasonable assumption if LP is indeed the priority behaviour): $120 million. Distribute that across the fewer than 5,000 wallets with over $100 in cumulative LP rewards and you get an average allocation north of $20,000 per wallet before any tiering that would skew further towards top LPs.

The numbers shift dramatically with different assumptions. At 10% of supply and 50% LP weighting the per-wallet figure for top-tier LPs could be multiples higher. Across a wide range of reasonable scenarios, the expected value per qualifying wallet exceeds the total cost of farming by a significant margin.

These are illustrative, not predictions. The point is that even the conservative end of the range produces a compelling multiple relative to the farming cost.

The key is ensuring the downside remains bounded. The entire strategy is designed around this constraint: profits from the initial phase fund the burn, rewards subsidise the cost, circuit breakers prevent blowups, and the total budget is sized such that a complete loss is tolerable.

We’re not betting the farm on an airdrop but rather spending a bounded amount on an asymmetric option.

What’s next

There are a few things I’m watching closely. Any changes to the Liquidity rewards program (adjustments to qualifying criteria or reward pool sizes) would warrant a reassessment of the strategy’s parameters. Similarly, any official communication from the Polymarket team regarding token timelines or eligibility criteria would reshape the calculus, potentially dramatically. And the competitive landscape: if Hyperliquid begins pulling the HIP-4 lever in earnest, Polymarket’s incentive to accelerate their own token launch increases which could compress the farming window.

As this piece goes to press, Polymarket has launched a referral program (30% revenue share on direct referrals) and introduced taker fees across nearly all market categories. A portion of these fees fund expanded maker rebates, providing an additional USDC subsidy to liquidity providers on top of the existing Liquidity Rewards, further reducing the net cost of being present. The introduction of taker fees has been controversial but for LP-focused strategies, the dynamic is inverted: fees are collected from takers and redistributed to makers, adding another subsidy layer to the economics of providing liquidity and confirming Polymarket’s internal focus on improving liquidity.

The first quarterly letter covering Q1 positioning and performance is coming in early April where I’ll be discussing what else has been taking place across the book and outlook into Q2. In the meantime, if you have questions or are running your own Polymarket strategy, I’d be interested to hear about it, don’t hesitate to reach out on X.

Interesting read, looking forward to seeing how this plays out