Q1 2026 Letter

Defensive Positioning, Offensive Mistakes

Q1 2026

Hepworth Iron Capital: -2.7%

S&P 500: -4.6%

BTC: -22.1%

Given that this is the inaugural quarterly letter, I do not have the luxury of pointing to prior letters to reference historical positioning so let me begin by giving a brief overview of how 2025 came to a close.

2025 was a good year with profit taking on core strategic positions and a series of shorter term tactical trades contributing to strong performance through year end. By mid Summer, I had become particularly disillusioned with the state of DATs and shifted to a more defensive posture. While this meant missing out on the final throes of the DAT mania, it enabled me to see the writing on the wall sooner than the average market participant, giving way to some profitable short positions in ETH and a smattering of alts through Q4. More importantly, shifting to a defensive posture allowed me to largely avoid a steep drawdown from the portfolio high watermark.

While this defensive posture broadly prevailed through Q1, I have started to selectively add back long exposure, but more on that later, let’s first discuss what did and did not work in Q1.

The Good

Coming into the year with a heavy stablecoin allocation has meant looking for opportunities to generate good risk-adjusted yield.

Despite broadly bearish market conditions there have been a few good spots offering some combination of good risk-adjusted real yield plus optionality in the form of points/future token incentives.

Concluded in late Q4/Q1:

Stable Pre-Deposit: pre-deposit campaign for a new Stablecoin-focussed Layer 1, realised at 28% annualised.

USDai: multiple real yield opportunities (looping, peg trading, Pendle LPs) while generating CHIP exposure, realised yield is yet to be seen as TGE looms closer.

opusIAUSD: a more niche capacity constrained opportunity realising 40% annualised.

LLP (+ LIT airdrop): farming the farmers via LLP which became less attractive post TGE, LIT airdrop was thanks to activity generated on Lighter through the year.

Ongoing:

USDG and GHO on Tydro: a bet on INK where even conservative assumptions make for an attractive risk-adjusted expected return.

Nado NLP: another way to bet on INK while being paid to take the other side of perp traders.

ONyc looped on Kamino: new and growing reinsurance protocol on Solana.

reUSD looped on Fluid: attractive real yield combined with points upside into Re TGE.

apxUSD and apyUSD Pendle LPs: likely the first STRC backed yield coin to TGE, Apyx Season 1 distributes 5% of supply over 12 weeks.

Payy: PR around recent fundraise opened the door to a token which was already looking likely based on the announcement of Payy Network.

Selective basis trading across venues

Polymarket (read more about the approach here, looking forward to providing an update in the next letter)

Future opportunities:

Saturn

Daylight

Variational OLP

Protocols have learned from past cycles and increasingly obscure the details of their incentive programs to prevent mercenary capital from gaming eligibility criteria. The result is that farmers are increasingly making allocation decisions with incomplete information: committing capital and time based on inferred rather than explicit reward structures.

The sweet spot is finding opportunities where the expected return based on conservative assumptions handily outweighs the estimated risk while trying to retain diversity across opportunities for risk management purposes.

The Bad & The Ugly

Unsurprisingly, all losses incurred this quarter have been associated with long exposure.

Attempting to take short-term long exposure in BTC has largely led to chop despite continued confidence in the structural view. Saylor’s STRC preferred equity instrument has been returning to par with increasing speed post dividend payments, attracting demand from fixed income ETFs and on-chain STRC backed yield coins are gaining traction. The thesis may still be correct, but expressing it as an outright long in a risk-off environment has been a mistake thus far. A relative expression (long BTC against a hedge) would have isolated the signal I was actually trading.

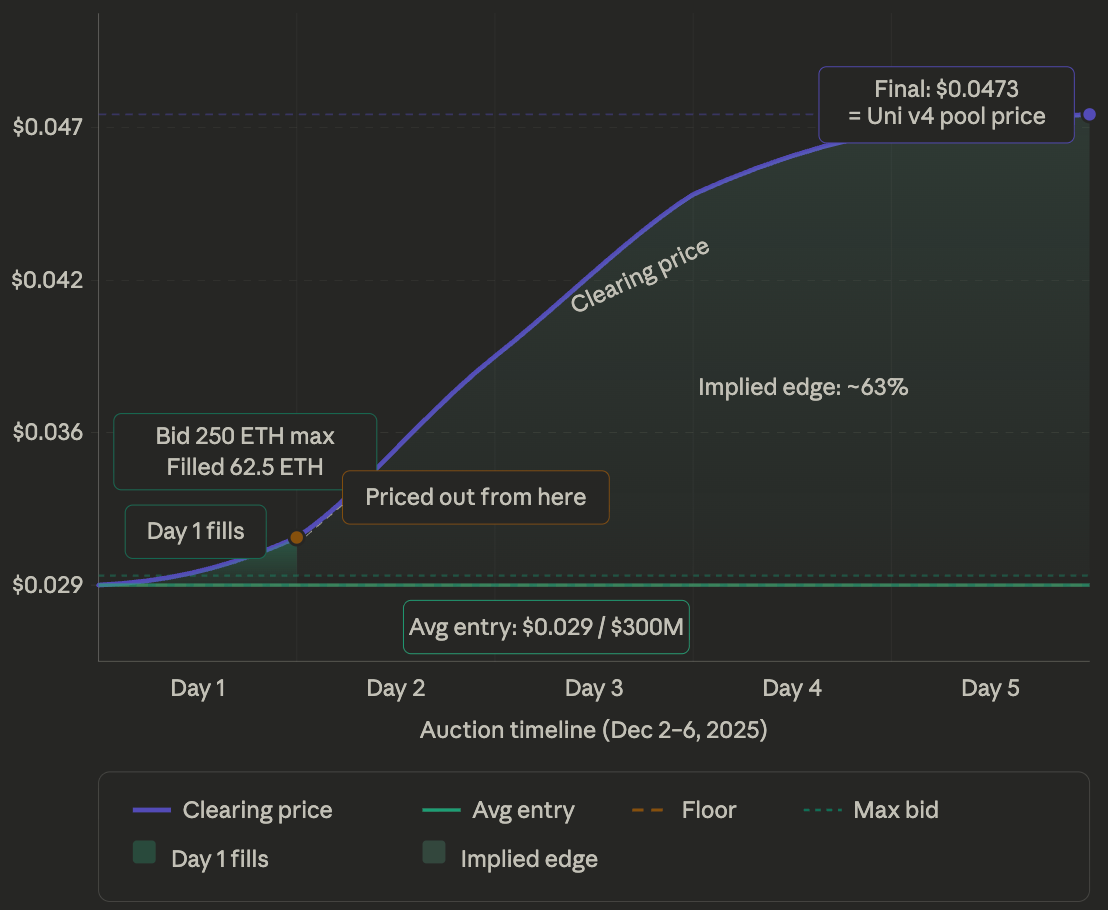

Other than getting chopped up on BTC, AZTEC has been the more interesting story. The idea was to play the wrinkles of the auction mechanics by participating in the Uniswap CCA on Day 1 of early bidding with a maximum sized bid at a price just above the floor. The CCA spreads bids across remaining blocks and clears each at a uniform price so by bidding early and low, fills concentrate in the cheapest blocks before later demand pushes the clearing price higher. Bid size matters here: if you assume the sale sells out, you know the clearing price will rise past your bid, meaning your order gets priced out after Day 1 and the remaining participants spend the rest of the auction buying above you. Max size at the floor maximises your fill in exactly those cheapest blocks.

The idea worked initially: with the average entry at $0.029, the auction cleared 63% above floor at $0.0473, which is also the price at which the Uniswap v4 pool launches at TGE. What I failed to foresee was the effect of a parallel reference price at TGE. Binance opened a pre-market which traded well below the CCA clearing level, creating block 1 MEV at TGE whereby any liquidity at the clearing price was taken instantly against the Binance price. The exit was not executed in block 1, the pool converged to Binance futures and the position was closed at a loss.

The two losses tell different stories. The BTC position was a case of reaching for directional exposure in an environment that didn’t support it. The structural thesis may prove correct in time, but expressing it as an outright long against a risk-off backdrop was the wrong trade at the wrong time. AZTEC was a different kind of error: the mechanical thesis played out exactly as designed, but I failed to map the full outcome tree at TGE, specifically the impact of a parallel Binance reference price on the Uniswap pool.

Two different errors, but the same lesson: in a quarter where the right macro call was to wait, the losses came exclusively from the trades where I didn’t.

Q2 Outlook

As alluded to, I have been selectively adding back long exposure throughout the quarter, for now this has been limited to HYPE and BTC.

HYPE is very well understood and my thesis is not unique or differentiated so I will not bore you with a bullish take here.

BTC is a little more interesting. Throughout the Iran war saga, BTC has failed to make new lows, showing significant resilience against broader risk. It has shown equal resilience through a fresh wave of quantum fears per Google’s paper. When an asset refuses to go down in the face of bad news, it is a sign of strength, signalling seller exhaustion.

Meanwhile, the structural STRC thesis outlined above remains intact, and the on-chain layer is accelerating. Saturn, the highest quality STRC-backed yield coin, is launching imminently. With Apyx already managing $100m+ TVL, Saturn could reach multiples of that.

Even if STRC is the only reason for the resilience in BTC, performance is performance and the relative outperformance we have seen could provide the seeds for a strong narrative if BTC starts to wake up a little here. The BTC long position taken in Q1 was likely premature but the stars seem to be aligning for better times in Q2.

I am actively monitoring other names and open to adding broader long exposure. I look forward to sharing ideas and deep dives here going forward.